Harmony in Allocating Inter-Departmental Power and Utilities Costs with the Three-Point Formula

Power and utilities best practices - the Three-point Formula

The 3-pointer? Do you mean in basketball or a field goal? Game winner? We could talk about all of these, but this topic is even more enjoyable. We're talking about the 3-point formula for allocating interdepartmental utility costs. Implementing a 3-point approach to allocating interdepartmental costs in a multi-service utility (electric, gas, and water, for example) can be comforting, especially if you remember your latest budget meeting and discussing allocating internal costs. This formula has been a proven industry standard since the 1950’s and is as true today as it was then. The formula can be used by a co-op or utility of any size - from $10 million in revenues to billions in revenues.

This article discusses how using a cost allocation method based strictly on math and metrics can smooth budget discussions. It doesn't sound exciting, but you'll be glad you checked this out.

Key article takeaways - the “Three-point Formula”

1. Cost allocation rules made simple - (1) direct charge a department whenever the cause and effect can be shown, and (2) use an industry allocation method for all remaining common costs

2. Cost that should be allocated to all company departments are "shared services." The customer of these shared services is internal to the organization.

3. The Three-point formula is a power and utilities industry standard used to allocate shared services. It is used by many electric cooperatives and utility organizations.

Allocating interdepartmental costs

The rules for allocating costs

There are two simple rules for allocating costs:

1. If your department causes a cost to occur, then the department should pay for the cost (aka, direct assign the cost to the department)

2. If rule #1 doesn’t apply, use an industry common method to spread (allocate) the cost

Simple, right? Maybe in theory, but you probably need more support than this. We’ll provide it.

Cost allocation theory

While the cost allocation rules are short and simple, cost allocation theory goes more deeply. Costs to be allocated should have these characteristics:

- Cost-causative: Relationship between the cause for the expense being incurred and the effect that the activity had on the benefiting business unit

- Measurable: Amounts from financial data – subject to internal controls and auditable

- Objective: Method should be determined without bias

- Stable/predictable: Methods should not produce variations that are not in line with service level variations

- Consistently applied: Cost per unit should be the same for all users of that service

The premise of the costs are that they should be allocated fairly and equitably. The great equalizer for that approach is math.

Shared services

Shared services are the costs that are alllocated to the different departments of the organization. These are services provided to internal customers, and so, must be paid for by the departments who are the customers of the services.

Functional characteristics of shared services include:

- High volume and routine transactions

- Specialized skills to provide the services

- Company-wide services delivery

Utility Accounting and Rates Specialists provides on-line/on-demand courses on operations and construction project accounting, rates, and management for new and experienced co-op and utility professionals and Board members. Click on the button to see a highlighted listing and description of our course offerings.

Functional areas to review for shared services

Departments that are candidates for inclusion in a shared services allocation include:

Information technology

Power dispatch

Customer service

Facilities

Fleet

Human resources

Finance

Purchasing

Many of these areas have the cost characteristics of being common and not critical to a specific utility department or service line. As in any case, directly assignable costs should be directly charged to a project or department, all others could be considered for a shared services allocation.

Three-point formula

The three-point formula is the secret sauce used to allocate interdepartmental costs. The formula is based on math and these industry drivers that determine the service level provided to internal customers, regardless of utility size:

1. Utility plant in service

2. Revenues

3. Total direct labor hours or full-time equivalents

The weighted average of these drivers of the utility business in a multiple service utility are calculated and used to allocate interdepartmental costs.

This formula has been used as a best practice since the 1950’s. The driver’s of service have been repeatedly analyzed and the Three-point Formula is still proven as the industry standard of allocations.

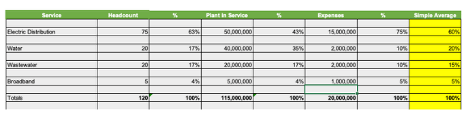

Example of the Three-point formula in action

This utility provides electric, water, and communications services to customers. The utility has not used the Three-point formula prior to now. Here’s how they calculated the Three-point formula:

Three-point Formula Calculation

[1] The weighted average for electric distribution is calculated as (63% + 43% + 75%)/3 = 60%

Upon performing the calculation, the utility would take these steps:

1. Direct charge any shared services costs to a utility if identified as caused by that utility

2. Allocate remaining shared services costs after they are pooled to electric distribution (60 %), water (20%), wastewater (15%) and broadband (5%).

The allocation for interdepartmental cost allocations used by the utility in prior years was 75%, 10%, 10%, and 5%. Budget concerns by the department heads for the water and wastewater utilities as to greater costs being allocated to their departments lead to a 2-year phase-in for the new allocation percentage.

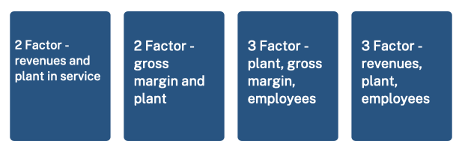

Other formula variations

There are other variations on the Three Point formula, such as:

Alternative Three-Point Formulas

Each of the above methods applies to a co-op or utility of any size, as the relationship between the factors remains relevant as the entity grows or shrinks its business.

Other allocation methods

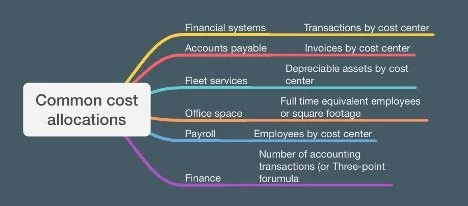

Other common cost allocation methods can differ by allocation area, but the allocation is generally driven by the activity. Below are common allocation methods for shared services:

Direct Cost Allocation Methods

Remember the allocation rules

There are two simple rules for allocating costs:

1. If your department causes a cost to occur, then the department should pay for the cost (aka, direct assign the cost to the department)

2. If rule #1 doesn’t apply, use an industry-common method to spread (allocate) the cost

These allocations directly impact rates for all utility services.

Will we have more productive budget meetings?

There are no guarantees that your department head budget meetings will be more productive. But, basing an allocation factor on industry standards and math is a very supportable position when allocating common interdepartmental costs.

What should you do next?

Calculate your co-op or utility's Three-point formula for allocating interdepartmental costs and compare it to your current allocation percentages.

1. Meet with department heads to discuss the calculation findings. Discuss the approach and industry standards, and get buy-in for a change.

2. Develop a transition plan for departments with significant changes from your current allocation method.

3. Develop a policy that details and documents your organization's approach.

4. Calculate the Three-point formula annually as part of the budget process and adjust as needed.

About Russ Hissom - Article Author

Russ Hissom, CPA is a principal of Utility Accounting & Rates Specialists a firm that provides power utilities rate, expert witness, and consulting services, and online/on-demand courses on accounting, rates, FERC/RUS construction accounting, financial analysis, and business process improvement services. Russ was a partner in a national accounting and consulting firm for 20 years. He works with electric investor-owned and public power utilities, electric cooperatives, broadband providers, and gas, water, and wastewater utilities. His goal is to share industry best practices to help your business perform effectively and efficiently and meet the challenges of the changing power and utilities industry.

Find out more about Utility Accounting & Rates Specialists here, or you can reach Russ at russ.hissom@utilityeducation.com.

The material in this article is for informational purposes only and should not be taken as legal or accounting advice provided by Utility Accounting & Rates Specialists. You should seek formal advice on this topic from your accounting or legal advisor.